The next logical step for category management

Recent radical changes in shopper behavior are putting pressure on category management practices to further adapt to the new dynamics of retail. How should reta...

How should retailers reinvent the center store?

For the past decade or more, supermarkets and their brand partners have frantically worked to devise new incentives to lure the shopper to center store. But any...

What does it take to thrive in an over-stored marketplace?

The over-storing of America is perhaps the most immediate and imposing problem facing retailers. Retailers need a radical change of focus and success metrics ai...

Why in-store merchandising has to change

At fixture and merchandising plan meetings attended over thirty-plus years, discussions centered on logistics and space availability, but there was little or no...

Is brick & mortar ready to leverage in-store shopper data?

Unlike their online counterparts, traditional retailers do not track the time spent in-store or engagement in their merchandising. Do you see brick & mortar sto...

Should sales guide pricing decisions?

As a battered veteran of many Monday morning retail meetings, BrainTrust Panelist Mark Heckman says that while sales growth is almost always discussed, it is se...

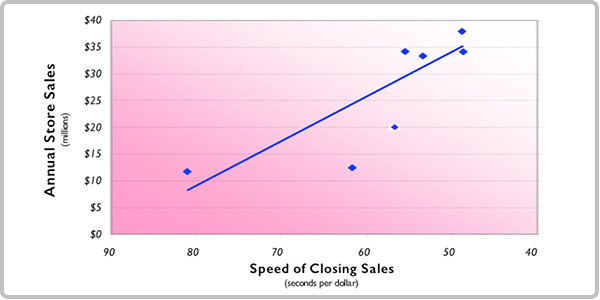

Making the case for shopper time management

Ask any retailer what their shopper's average trip length is or how fast shoppers buy once they are in one of their stores, and you will likely get blank stares...

Are stand-alone loyalty approaches anachronistic?

Well over 20 years ago, the first "electronic" card-based loyalty programs arrived to help retailers promote more effectively. With limited technology and inher...

Are retailers ready to deal with ‘Gargantuan Data’?

EBay's modeling predicts the amount of data available from online commerce transactions will double every year in the near term, a prediction has prompted eBay ...

How to draw a Big Data implementation roadmap

"Big Data implies that data sets are so large and complex they become awkward to work with using standard tools and techniques." Buried within this simple defin...